"Say Hello to

Independent Financial Advice"

0191 281 8811

Client Login

0191 281 8811

Client Login

How our emotional biases can affect our investing

We may not be aware of it, but our emotions can affect how and where we invest. Our emotional and behavioural biases can subvert our rational thinking and impact our financial decision making.

Whether investments are rising or falling, investors have a journey of emotions that, if allowed, can affect investment returns. This journey may be completely disconnected from actual stock market performance. Yet at each stage, we make trade-offs between immediate emotional comfort and long term returns.

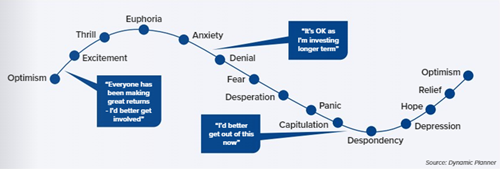

Below is a graph that typifies the investment journey of many investors, especially when investing for themselves. This graph shows the behavioural journey as stock markets rise and fall.

When markets are on the rise, we feel more encouraged to invest – experiencing optimism and then excitement as we see investments going up. But this can mean we buy when the markets and prices are high. Should markets fall, our emotions can turn to denial, fear and even panic as we see the value of our portfolio and our overall wealth fall, which can also drag down our expectations. This can prompt us to sell when prices are low.

Even when we know it is in the nature of stock markets to fluctuate, because we don’t know how long the upward and downward curves may last, we may take short term action based on fear or optimism.

There are a number of other behavioural biases that typically can affect financial decision making. Here are a few:

Negativity bias: Short term market falls can worry investors, especially where they are seeing their wealth decrease. Contrarily, short term increases are not viewed with the same level of emotion. Why is this? Behavioural finance theory suggests that the pain from a loss is felt twice as much as the pleasure from a gain.

Confirmation bias: This can be where we seek out information that supports an existing opinion, which increases our confidence to take a certain course of action. On the graph this might be the line between optimism and euphoria – where we look for news stories that support our view that markets will go up.

Recency bias: This is where we base our decisions for the future on recent events. This often comes from information that is easily accessible and available but which

can lead to poor investment choices. For example, seeing quick gains made on specific assets which lead us to think they will continue to do well.

Herd mentality: This is another bias. Leaping on a bandwagon because we see others doing it. The dotcom bubble of the late 1990s is a clear example of this, where investors piled into technology stocks, and sentiment drove up stock prices beyond true valuations until the bubble burst.

Anchoring bias: This is where we make decisions by relying on a single piece of information we hear on a topic. For example, we may hear that crypto currencies are the place to invest without investigating how they work or their risks.

Overconfidence bias: Where our subjective confidence overrides our objective judgement. For example, investors believing they can time the markets and investing on short term trends.

Do any of these biases resonate with you? Stock markets are driven by sentiment, which is why we have to avoid these biases wherever possible and put in place a rational, long term strategy.

Working with a professional financial adviser enables the creation of an investment portfolio that is specific to individual needs and financial objectives and establishes

a long term investment plan to follow, regardless of the market’s movements or the latest trends. Over our 50 years of helping clients invest, our professional investment team has seen market crashes and market rallies. Investors who have won out are invariably the people who have taken professional advice which has steered them away from these behavioural biases. Let us take care of your investments so you don’t have to.

Subscribe Today

Receive exclusive

financial insights

straight to your inbox

We will use the information you have provided only to contact you in accordance to terms of this contact form and our privacy policy.

You can unsubscribe at any time by emailing enquiry@lowes.co.uk or by clicking the 'unsubscribe' link at the bottom of each email. Full details of how we use and secure your personal information and how to update your marketing preferences can be viewed in our Privacy Policy.