"Say Hello to

Independent Financial Advice"

0191 281 8811

Client Login

0191 281 8811

Client Login

Phases of retirement

Retirees in 2016 were much better off financially than those who retired in 1977, a recent Government Survey has highlighted. Statistics indicate that income of the recent Retirees was as much as three times higher, having taken into account factors such as inflation. The main reason for this increase in incomes was the payment of private pensions to retirees.

We can certainly expect to live longer in retirement than previous generations, an ONS study in 2014 – shows that a 65 year old female would live on average an additional 23.7 years and that a male aged 65 could expect to live an additional 21.5 years on average.

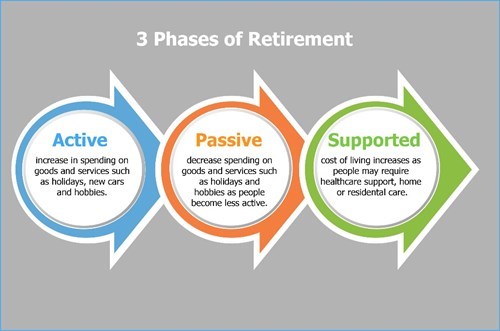

The way in which we spend our income during retirement will dictate how comfortably we are able to live. Our retirement choices are not only affected by our financial means but also by our health, family circumstances and our aspirations for this period of our lives. Retirement is generally broken into 3 phases for most people, in which spending is high initially, then dips, and then rises – often significantly – towards the final stages of life:

1) The Active phase – the most expensive phase of retirement is usually soon after a person retires, when they are often at their healthiest and making the most of their new leisure time. Individuals will typically spend money on goods and services such as new cars, holidays and hobbies. This period can typically last to age 75;

2) The Passive phase – in this phase, the rate at which we spend usually slows down as spending on discretionary items such as holidays reduces and people may become less active;

3) The Supported phase – as health deteriorates, many people can see costs increase if they require healthcare support such as nursing support or home help, either at home or in residential care. Health care costs are likely to take a large proportion of your savings if a succinct long-term care plan has not been determined.

It is important to remember that it is unlikely for us all to need the same level of income in retirement as is needed throughout our working life. Some individuals, once they retire, will be paying significantly less income tax, have no National Insurance (NI) or pension contributions to make, likely have paid off mortgages and loans, and have financially independent children.

Yet while some of our former outgoings may reduce, it is imperative to avoid spending too much money in the early years of retirement and being unable to afford to live comfortably through the rest of retirement.

Planning to retire with sufficient financial means is crucial and of course now needs to consider the increase in the age when we can start to receive the State Pension. Many people look to their pension for retirement income, but they should also consider other assets such as savings and investments as potential income sources. Financial planning, both pre and post retirement, should seek to not only maximise resources but also utilise available tax breaks and allowances, as doing so can help boost the funds available.

Subscribe Today

Receive exclusive

financial insights

straight to your inbox

We will use the information you have provided only to contact you in accordance to terms of this contact form and our privacy policy.

You can unsubscribe at any time by emailing enquiry@lowes.co.uk or by clicking the 'unsubscribe' link at the bottom of each email. Full details of how we use and secure your personal information and how to update your marketing preferences can be viewed in our Privacy Policy.

Request a Callback

To arrange a free, no obligation consultation or a call back from your Adviser, please complete your details and we will get back to you at the earliest possible opportunity. Alternatively contact us via:

A member of our team will use the details you have provided to respond to your enquiry.

You can unsubscribe at any time by emailing enquiry@Lowes.co.uk or by clicking the 'unsubscribe' link at the bottom of each email. Full details of how we use and secure your personal information and how to update your marketing preferences can be viewed in our Privacy Policy.