"Say Hello to

Independent Financial Advice"

0191 281 8811

Client Login

0191 281 8811

Client Login

On the QT

As we head into the final quarter of the year, politics remains firmly on the agenda.

Here in the UK, the negotiations around Brexit continue with party infighting about how the UK should approach this delicate situation. In Germany, Angela Merkel successfully held onto her role as Chancellor but the increasing popularity of right wing politics stood out.

Meanwhile, Donald Trump continues to air his views in the US but we are as yet to see any of the real promises made during his presidential campaign come to fruition. Finally, North Korea continues to test the patience of its neighbours with its continued missile testing. Whilst all of the above could have longer lasting consequences, for now markets appear to be considering these to be short-term noise.

Of more interest in the coming months will be the action of central banks, responsible for setting monetary policy around the world. In the US the Federal Reserve has now increased interest rates three times from their record low of 0.5% to their current level of 1.25%, however at its September however the Fed announced that it will also start to reduce the size of its balance sheet from this October.

Prior to 2008 few of us had heard of Quantitative Easing (QE) and when it was first implemented few understood the impact that it would have. Whilst the advantages and disadvantages which QE brought will be debated long into the future, one point which cannot be argued against is that, along with record low interest rates, QE brought an extended period of extremely accommodative monetary policy. Now, with the US economy on a firmer footing, growing at an annualised rate of just over 3%, unemployment at its lowest rate since 2001 at 4.2% and inflation just under 2%, the Federal Reserve is ready to reduce the size of its balance sheet. This is to be achieved by reducing the number of bonds they hold.

To provide a stable level of QE the central bank had been reinvesting the proceeds from the maturity of bonds they own back into new bonds. Between October and December this year, however, the Fed will reduce the level of money reinvested by $10 billion each month in what has become known as Quantitative Tightening, or QT. This has the potential to rise to $50 billion every month from next year until the balance sheet has reduced to $1 trillion in size. At $50 billion per month this may seem like a large amount of stimulus to be removed. With a current balance sheet of $4.5 trillion, it will clearly take some time to achieve their goal. Flexibility has also been maintained in that should the central bank believe that QT is having a detrimental impact of the economy then it can be reduced.

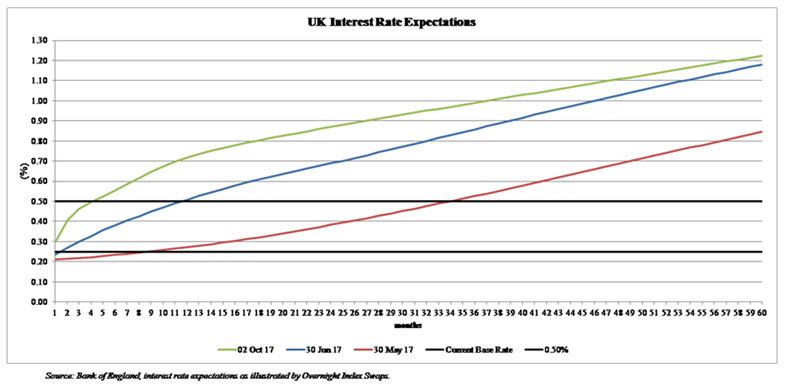

In the UK, however, Bank of England Governor Mark Carney has indicated that they will be in no hurry to reduce the size of their balance sheet. They are unlikely to do so until we have had a sustained period of rate rises. In the last few months the Bank has suggested that a rate rise may come sooner than initially expected following higher than expected inflation at 2.9%.

In the chart above we show the expected path of UK interest rates over a period of 5 years from each date stated based on interest rate transactions between banks. Expectations in May and June were that the first rate rise was still some time away. Following Carney’s more recent comments however it is anticipated that a 0.25% increase could come towards the end this year or the beginning of next. Note however how low expectations remain further into the future.QE had a positive impact on the returns achieved by many assets classes as investors were encouraged to take exposure to riskier asset classes to achieve their return objectives. As this partially unwinds via QT we will monitor closely the reaction markets make. We are yet to see any signs of the taper tantrum of 2013.

Subscribe Today

Receive exclusive

financial insights

straight to your inbox

We will use the information you have provided only to contact you in accordance to terms of this contact form and our privacy policy.

You can unsubscribe at any time by emailing enquiry@lowes.co.uk or by clicking the 'unsubscribe' link at the bottom of each email. Full details of how we use and secure your personal information and how to update your marketing preferences can be viewed in our Privacy Policy.

Request a Callback

To arrange a free, no obligation consultation or a call back from your Adviser, please complete your details and we will get back to you at the earliest possible opportunity. Alternatively contact us via:

A member of our team will use the details you have provided to respond to your enquiry.

You can unsubscribe at any time by emailing enquiry@Lowes.co.uk or by clicking the 'unsubscribe' link at the bottom of each email. Full details of how we use and secure your personal information and how to update your marketing preferences can be viewed in our Privacy Policy.